Important 2025 Shield Plan Update — What You Should Consider Before Adjusting Your Coverage

Nov 18, 2025 6:55 am

Hi ,

Hope you have been well. I am reaching out with an important update that affects almost everyone with an Integrated Shield Plan (IP).

The Straits Times recently reported that six out of seven insurers in Singapore have increased IP and rider premiums for 2025, mainly due to higher claims, rising medical costs, and expanded benefits.

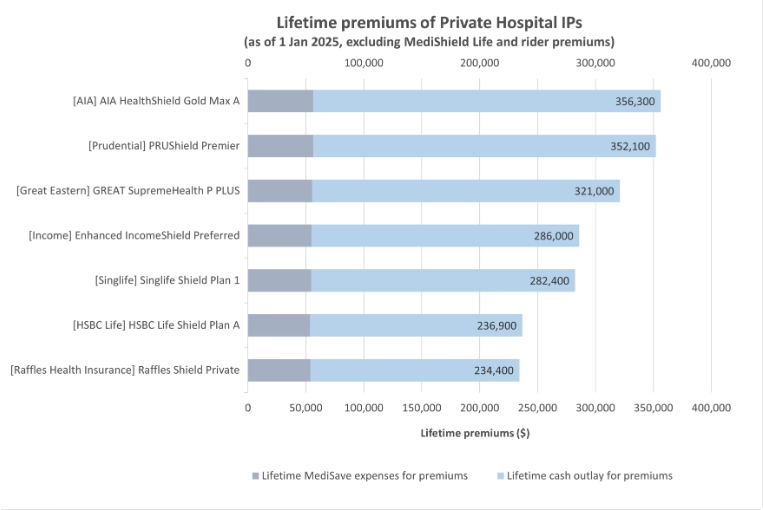

To help Singaporeans make better decisions, MOH also released a comparison of lifetime premiums for Private Hospital IPs:

What this shows:

- Lifetime premiums differ significantly across insurers

- Premiums rise the fastest from age 45–75

- A small annual increase compounds into a big difference over time

It’s normal to feel concerned about rising premiums, but decisions about your coverage should not be based on price alone.

Before adjusting your plan, here’s something important to consider

Some clients tell me:

“Maybe I’ll just downgrade to save money.”

Cost is important, but a recent Straits Times article highlights why it’s also important to consider timeliness of care.

A woman, Madam Tan, waited five months for a colonoscopy appointment at SGH.

https://www.straitstimes.com/singapore/health/woman-turned-to-private-sector-as-she-had-to-wait-5-months-for-colonoscopy-at-sgh

Fearing cancer, she did not want to wait.

She went to private specialist Dr Desmond Wai at Mount Elizabeth Novena:

- He saw her within days

- Did the colonoscopy within the week

- The results unfortunately confirmed her suspicion — she had advanced colon cancer, which had already spread to her liver

This story isn’t meant to create fear, but it shows something crucial:

➡️ Sometimes timely access to diagnosis and treatment matters just as much as cost.

➡️ Different plans give you different pathways to care.

This is why it’s important to review not just premiums but also your coverage needs and preferred access to care.

How Shield Plan comparison has changed (2025 landscape)

With full riders largely phased out, the key comparison points now are:

In simpler terms, what matters now:

- How easy it is to cap co-payment (panel criteria, emergency situations)

- Whether co-payment can be capped even without riders

- Availability of panel specialists across private hospitals

- Whether claims-based pricing applies

- CDL and non-CDL drug coverage

- Track record of premium stability

- Long-term affordability based on your age group

These vary widely across insurers.

If you’re open, I can help you check:

- How your premiums may move in the next 5–15 years

- Whether your current rider still gives good value

- Whether your current plan still matches your real healthcare needs

- How your plan compares using MOH’s latest reference data

- Options to maintain strong coverage while managing premium increases

- Whether downgrading or adjusting coverage makes sense for your situation

If you would like me to run the numbers for you, simply reply “Review” and I’ll drop you a text.

Warm regards,

Zest

Executive Wealth Consultant

Infinity Financial Advisory

DISCLAIMER;

This message contains privileged and confidential information from Infinity Financial Advisory Pte Ltd. If you are not the intended recipient of this electronic message, please do not disseminate, copy or take any action in reliance on it. We request you notify us immediately before deleting this message. Any views expressed in this message or attachment/s are those of the individual sender and are not necessarily the views of the company. Infinity Financial Advisory Pte Ltd uses virus scanning software and while due care and attention is taken; the company excludes all liability for any loss or damage caused whether directly or indirectly by any computer virus or other defects transmitted with any email and any attachment(s), to the extent permitted by law. It is sent on the strict condition that the user carries out and relies on its own procedures for ensuring that its use will not interfere with the recipient's systems including but not limited to scanning this email and any attachment(s) for viruses and defects before opening or sending them on. The recipient assumes all risk of use and releases the sender from all responsibility and liability for any direct or indirect consequence of use.