Why policy wording matters in a critical illness claim

May 05, 2026 8:15 am

Hi ,

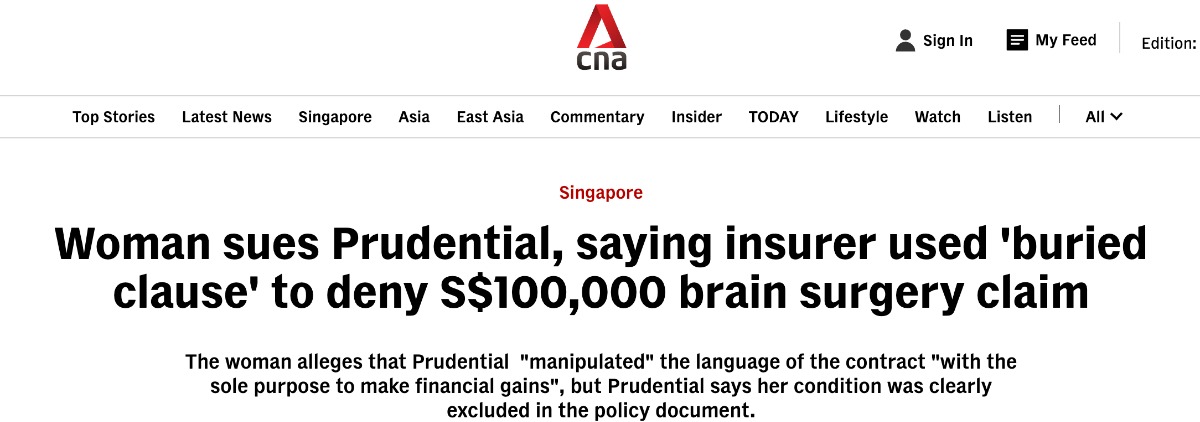

You may have seen the recent news about a policyholder disputing a critical illness claim after suffering a brain aneurysm.

I thought it was worth sharing because it highlights something important:

When it comes to critical illness coverage, it is not enough to know that a condition is listed in the policy.

The actual payout depends on how that condition is defined.

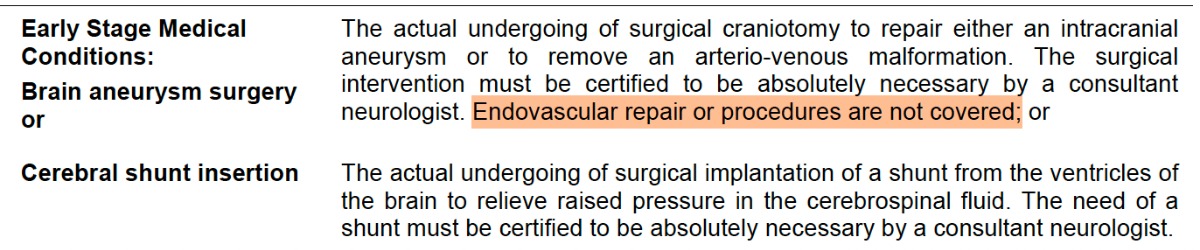

This issue arose as Prudential's policy definition for brain aneurysm surgery stated that the condition must involve surgical craniotomy, meaning open-skull surgery. It also excluded endovascular repair or procedures.

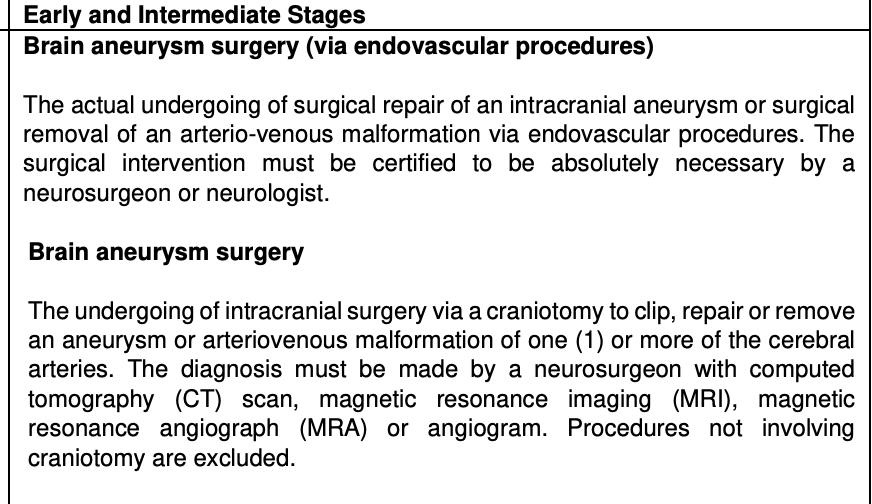

By comparison, another insurer’s definition has a separate section that recognises brain aneurysm surgery via endovascular procedures, subject to the exact policy terms and claim assessment.

This difference may look technical, but it can matter greatly at the claim stage.

Two policies may both appear to cover “brain aneurysm”, but the actual payout outcome can differ depending on the treatment method, severity, and how the condition is defined in the contract.

This is also why working with a multi-provider adviser can be valuable.

Different insurers may define the same condition differently. Some may have broader wording in selected areas, while others may be more restrictive depending on the condition, stage, or treatment method.

Because we have access to multiple insurers, we are not limited to one company’s product range. This allows us to compare across providers and recommend a plan based on your needs, budget, health profile, and the quality of the coverage wording, not just the premium or sum assured.

That said, definitions will still differ from insurer to insurer. No policy covers every situation, and every claim is still assessed based on the exact contract wording and medical evidence.

So it is always good to review your existing coverage from time to time, especially if your policy was bought many years ago.

A review can help you understand:

Whether your current critical illness coverage is still relevant

How strict or broad the definitions are.

Whether newer plans may offer broader wording in selected areas

Whether your coverage amount is still enough today

This is not about buying more insurance for the sake of it.

It is about knowing what you are actually relying on before a claim happens.

If you would like me to help you review your critical illness coverage, feel free to reply to this email or WhatsApp me.

Warm regards,

Zest

Executive Wealth Consultant | Associate Estate Planning Practitioner |

Licensed General Insurance Advisory

DISCLAIMER;

This message contains privileged and confidential information from Infinity Financial Advisory Pte Ltd. If you are not the intended recipient of this electronic message, please do not disseminate, copy or take any action in reliance on it. We request you notify us immediately before deleting this message. Any views expressed in this message or attachment/s are those of the individual sender and are not necessarily the views of the company. Infinity Financial Advisory Pte Ltd uses virus scanning software and while due care and attention is taken; the company excludes all liability for any loss or damage caused whether directly or indirectly by any computer virus or other defects transmitted with any email and any attachment(s), to the extent permitted by law. It is sent on the strict condition that the user carries out and relies on its own procedures for ensuring that its use will not interfere with the recipient's systems including but not limited to scanning this email and any attachment(s) for viruses and defects before opening or sending them on. The recipient assumes all risk of use and releases the sender from all responsibility and liability for any direct or indirect consequence of use.